You’ve Been Granted ISOs; Now What?

By James McDougal, CFP®| June 22, 2026 | Updated July 7, 2026

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax rates and IRS rules are subject to change; consult a qualified tax professional before making decisions about your equity compensation.

TL;DR:

Watch Out for the AMT Trap: Exercising and holding your ISOs can trigger the Alternative Minimum Tax (AMT) on "phantom income" (the spread between your strike price and the fair market value), meaning you could owe taxes on value you haven't cashed out yet.

Timing Dictates Your Tax Bill: To unlock optimal tax treatment (Long-Term Capital Gains), you must hold your shares for more than 2 years from the grant date and more than 1 year from the exercise date. Selling any sooner triggers a Disqualifying Disposition, hitting you with ordinary income tax rates.

You Are Your Own Tax Withholder: There is zero payroll withholding when you exercise or sell ISOs. You are entirely responsible for tracking your transactions and setting aside cash to pay the tax bill.

Look for Extra Upside: Early-stage startup employees should check if their shares are QSBS (Qualified Small Business Stock) eligible, which can exclude up to $10M or $15M in gains from federal taxes. Additionally, any AMT paid can be recovered in future years through the Minimum Tax Credit.

Congratulations on your ISO grant! You’re officially part of the growing cohort of Americans who have to figure out what acronyms like AMT mean and whether you’re going to have a breakdown when your CPA hands you your tax return next year.

Maybe this isn’t your first time, but you may still feel like you’re at square one in making the most of your ISOs. You’re not alone! This stuff is complex, but if you were talented enough to receive your ISO grant in the first place, you’re talented enough to develop a wise and thoughtful plan for it.

Does your grant have an ISO/NSO split? Check out our What You Should Know About NSOs blog post.

What Are Incentive Stock Options (ISOs)?

Incentive Stock Options, or ISOs, are a form of stock option agreement designed to offer equity ownership to employees of US-domiciled C Corporations with key tax incentives. ISOs function as all ordinary ‘call’ options do, where the option holder is given the right—not the obligation—to purchase a fixed number of shares in a company at a set price with a predetermined expiration date.

Ideally, you’re one of the lucky few who get to exercise your options at a purchase price lower than the stock’s fair market value, recognizing a gain between your strike price, or purchase price, and the stock’s Fair Market Value (FMV). Conversely, you may find yourself in a position where you’ve exercised your ISOs, but the FMV never surpasses your exercise price. You may also be in a position where you’re able to sell your options in a cashless exercise.

Understanding how you got here, how and when you choose to transact, and the tax impacts along the way are the key to unlocking your ISOs. These waters can get muddy very quickly, but I promise you’ll be treading water by the end of this article!

Context Is Everything

Understanding what makes ISOs unique can be like trying to bite into a tall, delicious sandwich; we’ll take our first bite by understanding the importance of context. ISOs are typically granted by non-public companies for the benefit of early employees. Because you’re likely at an early-stage company, you’re facing a unique and often difficult-to-parse set of facts regarding industry and company risk, your prospects for staying with this company, liquidity, and future share price, to name a few. These factors carry weight and real consequences, and a thoughtful plan should account for them. Sitting amidst this jumble of factors is a unique set of tax implications, which we’ll spend some time understanding now.

For the sake of this article, let’s assume your company is well-positioned and you have the cash and appetite to put some skin in the game. What are the tax implications of pulling the trigger on your ISOs?

Is your company granting RSUs as well? Check out our Getting A Grip On Restricted Stock blog post.

Taxation of ISOs

Keeping with our sandwich analogy, the tax law piece of ISO planning is a big bite and requires slow, patient chewing. We’ll take this chronologically from grant to exercise to sale and explain the tax implications at each step.

At grant and eventual vest, you should not expect tax consequences as a result of either; your priority at this stage should be planning for eventual exercise, which is where the tax considerations start to come into play. Once your options are vested (or you’re able to early-exercise) and you have a way of funding the cost to exercise, it’s time to start planning for the Alternative Minimum Tax (AMT) bill you may inadvertently rack up.

Will I Owe AMT If I Exercise My ISOs?

Alternative Minimum Tax (AMT) is derived from a separate tax calculation that counts the spread between the strike price and fair market value (bargain element) of your ISOs as income. If your tax liability under the AMT calculation exceeds your ‘regular’ tax liability, you pay the difference. This is one situation in our tax code where you can owe tax on ‘phantom’ income, or taxable income that doesn’t produce earnings in a traditional sense.

It’s important to understand that if your strike price and fair market value (409A valuation typically) are equivalent, there is no bargain element for AMT purposes. In cases where there is a significant spread between the two, you should meet with your financial planner or tax advisor to map out a range of breakpoints in your exercise strategy. HiFi Planning takes a choose-your-own-adventure approach, where AMT implications are demonstrated alongside a range of exercise scenarios and weighed against broader financial planning concerns.

Exercising ISOs can be exhilarating and life-changing, but it’s essential not to lose sight of questions like “where am I going to get the cash to pay the exercise cost and/or tax bill” or “what happens if my stock never becomes liquid?”

Now that we’ve completed our crash course in AMT, we need to understand what happens when you sell the shares you’ve exercised.

What Are the Tax Implications of Selling My ISOs?

Sales of ISO-derived shares fall into two categories: Qualifying and Disqualifying dispositions. Each carries their own implications, so we’ll start with Qualifying Dispositions (QDs).

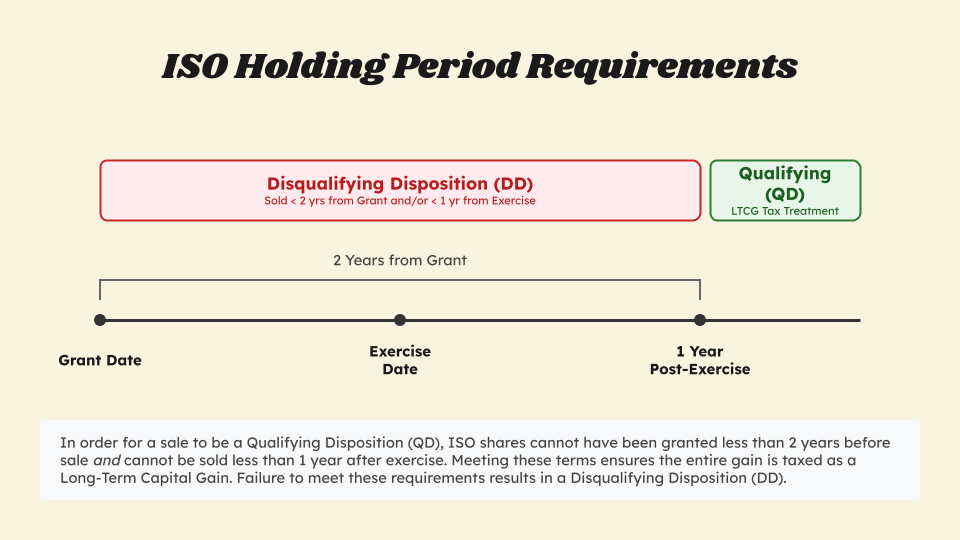

In order for a sale to be a QD, the seller must meet specific holding period requirements. ISO shares sold cannot have been granted less than 2 years before sale and they cannot be sold less than 1 year after exercise. Assuming these terms are met, the gain (spread between strike price and sale price) is taxed entirely as a Long-Term Capital Gain. This is where the tax benefits of ISOs can really come into play. If these holding period requirements are not met, you’re looking at a Disqualifying Disposition (DD).

In a DD, you’re taxed on the spread between strike price and FMV on the exercise date as ordinary income, and any gains in share price above that exercise date FMV are taxed as Short- or Long-Term Capital gains according to the time between exercise and sale.

If you're a visual learner, here is a quick look at how the clock ticks on your ISOs:

ISO Disposition Timeline

To further illustrate how these timelines change your tax rates side-by-side, see the quick-reference guide below:

| Disposition Type | Holding Period Requirement | Tax on Spread (Strike to Exercise FMV) | Tax on Growth |

|---|---|---|---|

| Qualifying (QD) | > 2 years from grant AND > 1 year from exercise | No Ordinary Income tax at exercise; option spread is AMT add-back item | Difference between Sale Price and Strike Price taxed as Long-Term Capital Gain |

| Disqualifying (DD) | Sold before meeting QD timelines | Ordinary Income | Difference between Sale Price and Exercise FMV taxed as Short or Long-Term Capital Gain |

Here are a few examples to illustrate how holding periods can play out:

Qualifying Disposition:

Charlie Bucket is granted 5,000 ISOs in Wonka Corp. on 1/1/2024 with a strike price of $1.

As soon as he’s met his 1-year vesting cliff, he exercises 1,250 ISOs when the company’s 409A value is $2/share.

He sells these exercised shares in a tender offer on 3/31/2026 at $3/share. For tax purposes, he will recognize the $2 spread between sale price and strike price as Capital Gain income, meaning he will recognize a $2,500 Long-Term Capital Gain on his tax return. Talk about a golden ticket!

Disqualifying Disposition:

Veruca Salt is also granted 5,000 ISOs in Wonka Corp. on 1/1/2024 with a strike price of $1.

She doesn’t exercise any ISOs prior to the tender offer in 2026, at which time she has 2,500 vested ISOs.

She sells all of her vested ISOs in a same-day sale transaction at $3/share. She will recognize the $2 spread between strike price and FMV as Ordinary Income on her tax return. Still a lucky break for this bad egg, but she’s likely paying more in tax than Charlie.

Another Disqualifying Disposition:

Mike Teavee is granted 5,000 ISOs in Wonka Corp on 1/1/2025 at a $1 strike price, and due to his short attention span, he’s given an early-exercise provision, where he can exercise ISOs before they’ve vested.

He exercises all 5,000 ISOs as soon as he can get enough cash together On March 1, 2025 with a $2 409A valuation. He also files a timely 83(b) election after consulting with his trusted CFP® Professional at HiFi Planning. Note, he will recognize income for AMT on the option spread in the year of exercise.

By March 1, 2026, 1,250 of his shares have vested, and he decides to sell them in the tender offer in a Disqualifying Disposition on March 31, 2026. Despite holding onto his exercised shares for over a year, he’s still in DD territory due to selling less than 2 years after grant. He’ll recognize the $1 spread between strike price and exercise date FMV as Ordinary Income in the year of sale, and will also recognize the $1 difference between exercise date FMV and sale price as a Long-Term Capital Gain. We’ll see how far he can stretch these proceeds.

That was a big bite, so I hope you’re chewing slowly! In case that wasn’t enough to consider, there are a few other common planning tidbits when building exercise strategies that I want to lay out.

Why Would I Disqualify My ISOs?

If you’re in a position where your stock’s FMV has dipped below your exercise price, you may find yourself in a position where you owe AMT on value that no longer exists. For ISO exercises where AMT is generated, holding those shares beyond the calendar year of exercise requires you to pay AMT by the following April tax deadline—period. Conversely, selling exercised ISOs in a DD in the same calendar year can strategically eliminate this AMT bill.

Will There Be Withholding on My ISOs?

For all ISO transitions, expect no payroll withholding on exercise or sale. Payroll withholding and ISOs tends to be a point of confusion, especially in cases where ISO grants are split into ISOs and NQOs due to the $100,000 rule.

This means you’re in charge of cataloging your ISO transactions and calculating and paying any tax liabilities generated by them. It gets even more fun (complicated) when you consider the fact that ISO gains are exempt from Social Security and Medicare taxes. Your financial planner or tax advisor should be able to help you understand how the various tax liabilities add up in your specific circumstances.

What Do I Do If My ISOs are Qualified Small Business Stock (QSBS) Eligible?

For the uninitiated, Section 1202 of the US tax code lays out a framework for excluding up to $10M or $15M in gains on the sale of Qualified Small Business Stock (QSBS). For employees of very early-stage startups, there’s a good chance your shares will count as QSBS.

If this sounds like you, it’s imperative you connect with a qualified financial planner and/or tax professional to make sure you’re crossing your T’s and dotting your I’s. QSBS comes with its own set of holding period requirements and state tax implications, and is often one of the least-understood areas of tax planning. Missing out can result in significantly over-paying in taxes on your exit. Many financial planners versed in equity compensation have horror stories to share!

Getting Cash Back through Minimum Tax Credit

Key to optimizing your ISO exercise strategy is the Minimum Tax Credit: the mechanism by which AMT you pay in a given tax year can be ‘paid’ back to you in the form of a tax credit in the years following.

At a glance, you generate Minimum Tax Credit by paying AMT, and you capture this credit in years following where your ‘regular’ tax liability exceeds your AMT liability. This credit can be captured in pieces over a handful of years or all at once, but the important thing is that it’s being captured. By far, this is the number one thing that gets missed in ISO planning and reporting.

If you’ve paid AMT in a prior year, make sure you shout it from the mountain tops!

HiFi Has You Covered

We’ve taken quite a few big bites of our sandwich, but you may still be wondering how this applies to your unique situation. If you’re ready to unlock the potential in your ISO strategy, HiFi Planning is here to help. Schedule a free Discovery Call today to take control of your equity compensation package!